.png)

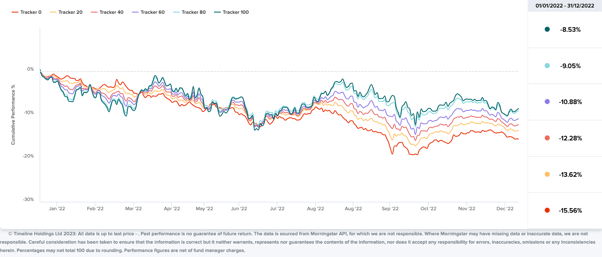

Bonds, which are universally considered safer assets, fell more than equities. A global bond portfolio fell by 16% in 2022, compared to a 9% decline in a global equity portfolio. And to add insult to injury, inflation is biting hard with CPI at over 10%, the highest in my lifetime. The implication is that a global bond portfolio is down as much as 25% in real terms in the past year. Ouch.

As brutal as that sounds, the investment market did exactly what it’s meant to do in 2022. If your investment horizon is dictated by how long it takes the sun to revolve around the earth, you should never have been in the markets anyway. If it’s a decade or longer, you’re still quids in. A globally diversified portfolio isn’t just for Christmas, it is for life.

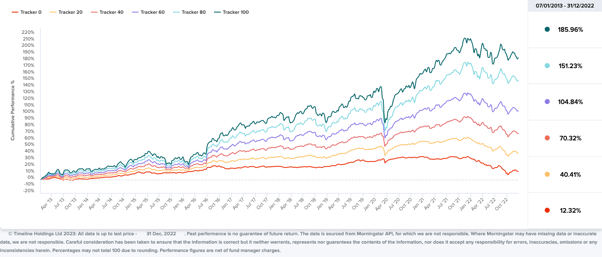

Over the past 10 years to the end of 2022, a globally diversified equity portfolio has returned a whopping 185%. Even a 60/40 equity/bond portfolio has returned a not too shabby 104%.

The enduring investment lesson of 2022 is that time in the market is the superpower, not timing the market. The longer your time horizon, the better.

Another takeaway from the past year is that your point of reference matters. If your investment thesis is based entirely on the last 20 or even 40 years, you probably got a nasty surprise. If you base your thesis on a 100+ years however, the returns of 2022 fits into the range of outcomes within that dataset.

In the past year, we saw inflation and bond yields rising to levels not seen in nearly half a century. If you extend your reference point to a 100 years however, the inflationary environment of 2022 is hardly unprecedented.

Many people are making a big deal of the fact that both equities and bonds posted a negative return in 2022. However, If you look at every 12-month scenario since 1900, it turns out that 1 in 10 scenarios ended up with bonds and equities posting a negative return in nominal terms. If you adjust the returns for inflation, 1 in 5 scenarios ended up with negative returns for both equities and bonds.

We’ve always extolled the virtues of stress-testing your financial plans using extensive historical data to illustrate a wide range of scenarios. Why wouldn’t you? Everybody has a plan until they get punched in the face. Stress-testing your plan with a century of data doesn’t necessarily prevent the punch. It does prepare you for it though. And the longer the dataset, the more scenarios you’re able to stress-test and prepare for.

Humans have short memories. And that’s why we have data. Much of the surprises we get when it comes to investing is due to having a narrow term of reference, that is based on a decade or two. Once you expand your frame of reference by a century of data, there’s hardly anything new under the investment heavens.

.png)