Commodities are classed as “alternative” investments. Unlike “financial” or “traditional” assets such as bonds and equity, commodities are physical assets that produce no cashflows and may incur storage and transportation costs.

Overview and Valuation

Commodities are classed as “alternative” investments. Unlike “financial” or “traditional” assets such as bonds and equity, commodities are physical assets that produce no cashflows and may incur storage and transportation costs.

This makes determining the fair value of commodities difficult. In simple terms, the standard approach to valuing financial assets is to forecast all expected cashflows, be it interest payments or dividends. For each expected cash flow, we apply a “discount rate” based on the risk of the investment and increase the impact of this discount rate as cashflows extend further into the future. This gives us the current value of the investment.

Instead, the current, or “spot” price of a commodity can be viewed as the discounted selling price of the commodity at some time in the future. Storage costs for commodities often result in forward prices that become higher, the longer the time until the commodity is due to be sold.

The simplest way an investor can gain exposure to commodities is to buy and hold the commodity themselves. This will not always be practical. Although some commodities are easy to buy and store, for example, gold (albeit in small quantities), buying and storing gas or livestock would be difficult and expensive for most investors. Also, the investor would likely find it difficult to hold a diversified portfolio of commodities.

Because of this, one of the primary ways investors gain diversified exposure to commodities is via commodity funds that use financial instruments called futures. Futures are essentially contracts that allow producers and buyers to lock in a price, to remove uncertainty. For example, a farmer may wish to guarantee the price he receives for the grain that will be harvested next year. At the same time, a baker may want to lock in the price he will pay for the grain to make bread. Each will enter into a futures contract today to agree on the price in the future. When this contract expires, if the current price in one year is not the same as the futures prices that were agreed by the buyer and seller, one will be worse off. For example, had the farmer agreed to sell his grain for £100 but a year later, grain in the market is trading at £250, the farmer effectively loses out by £150.

The commodity fund essentially speculates on the future price of commodities by forecasting supply and demand and then takes positions in futures contracts, hoping to benefit from those anticipated movements. Long term results are based on the consistency and accuracy of the fund managers’ predictions.

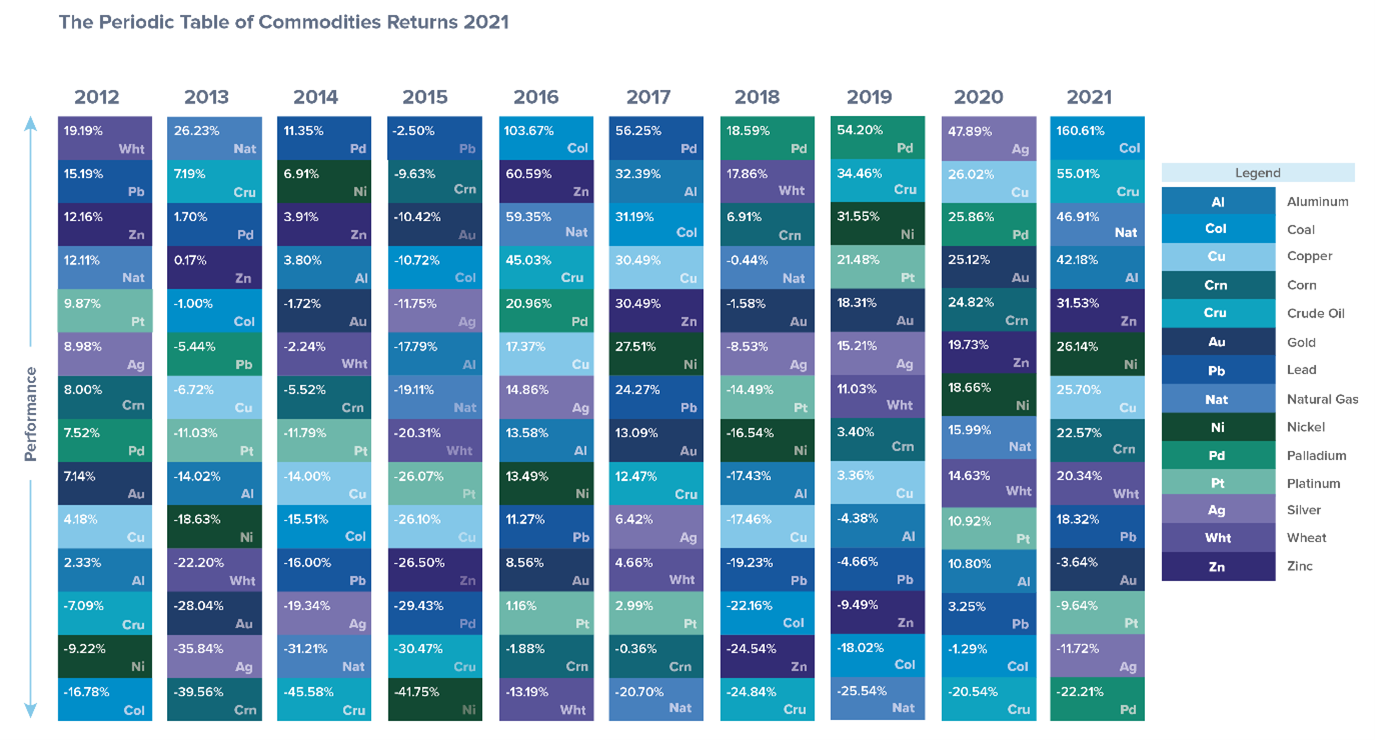

It’s important to understand that “commodities” includes a wide range of sectors, and although commodities as a whole may have performed well in comparison to bonds and equity in recent times, individual commodity sectors over time have not performed consistently. This is because the factors that influence supply and demand, plus the nature of production differ for each commodity sector.

The chart below serves to illustrate the inconsistency of returns between commodity sectors.

Source: US Global Investors (2022)

Inflation Hedge?

Commodity prices are essentially driven by the law of supply and demand. For example, if supply drops due to sanctions on Russian oil, but demand remains constant or increases, it will result in price increases. This is because commodity prices tend to rise during periods of inflation, and investors have traditionally seen commodities as protection, or as a “hedge” against inflation.

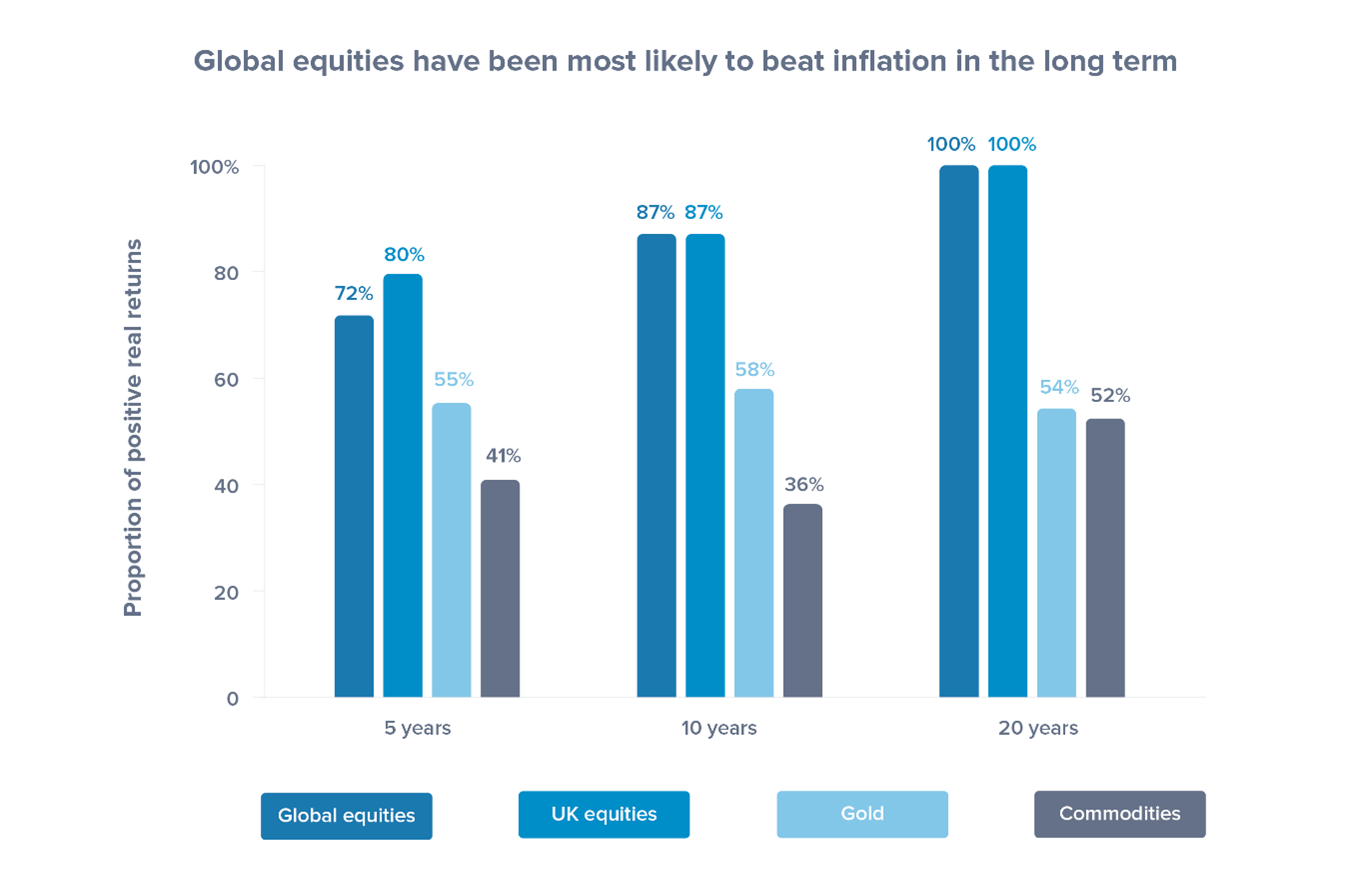

Are these investors, right? Yes and no. Over short-term horizons, equities have not historically been a good inflation hedge. However, where equities come into their own, as so often the case, is over the long term. If investors want to give themselves the best chance of growing their wealth, in excess of inflation, holding equities over the long‑term is the best strategy. This is reflected in the chart below. Over 5-, 10- and 20‑year periods, the chance of achieving a positive real return is far higher by investing in equities, rather than commodities.

Source: Vanguard (2021) The chart shows the proportion of real five-, 10- and 20-year returns that have been above 0%. The sample period for the monthly data is 31 January 1975 to 31 October 2021. Volatility is calculated over monthly returns of the entire sample period. Sources: Vanguard calculations in GBP, based on data from Bloomberg and the OECD.

Vanguard (2022)

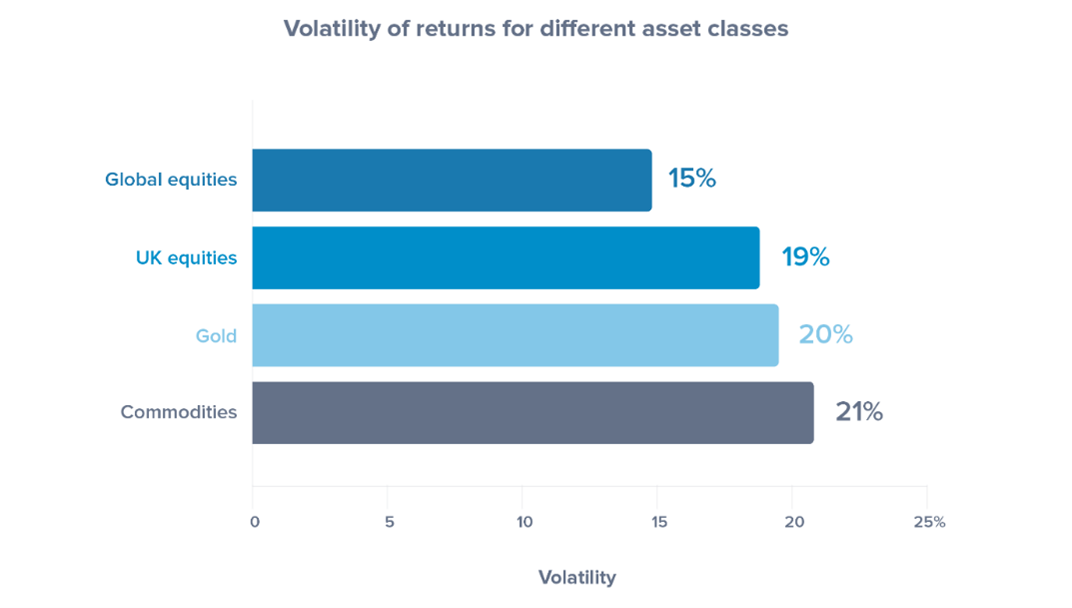

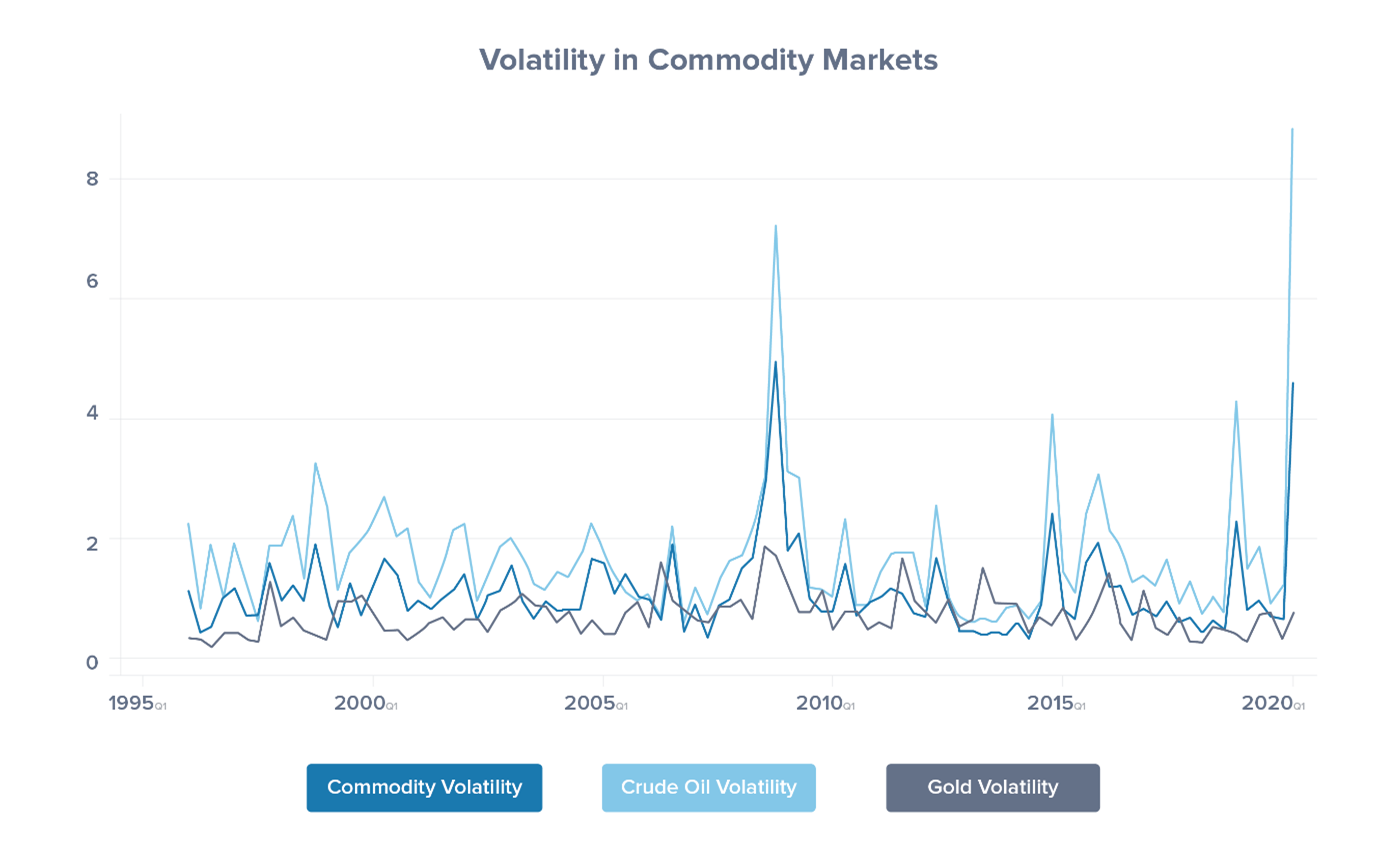

It’s not just the long term returns of commodities compared to equities that make them less attractive as an inflation hedge. It’s also the volatility of returns. This can be seen in the chart above; commodities had the greatest volatility of returns over the 46-year sample period.

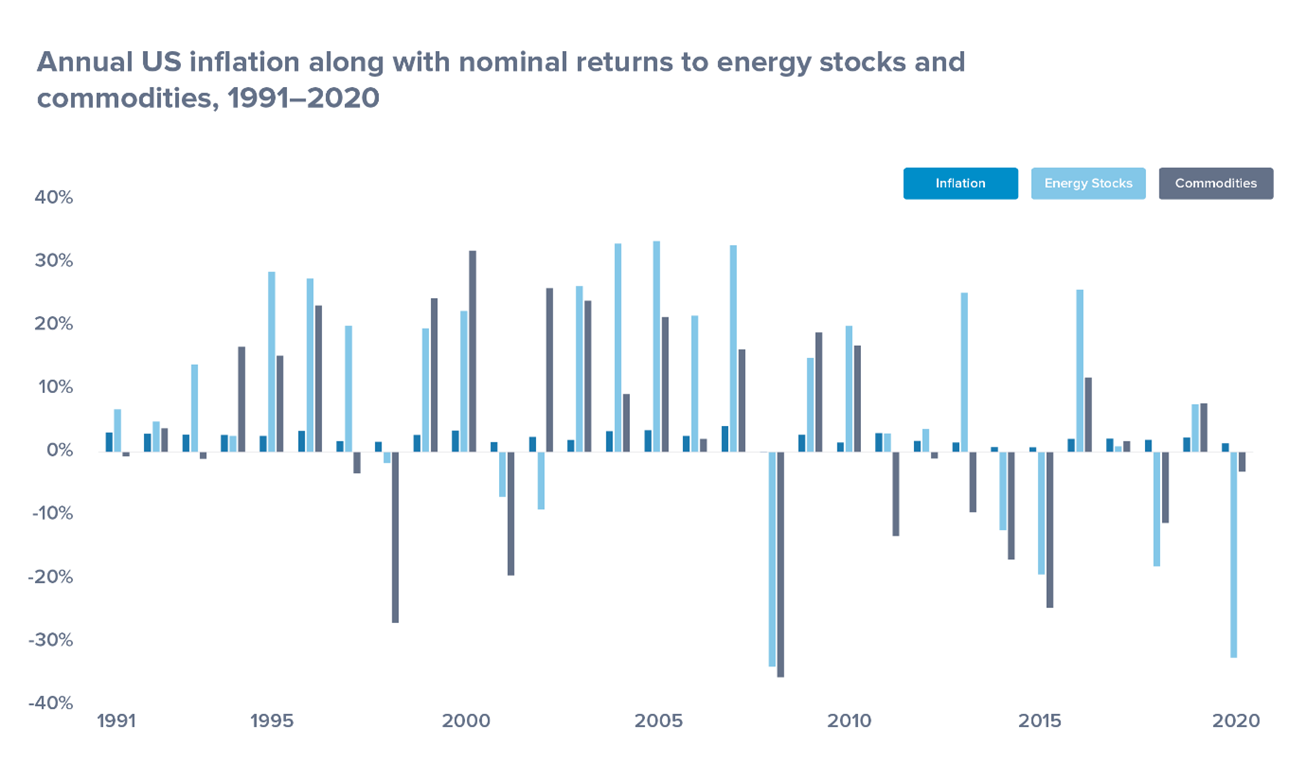

While nominal returns of energy stocks and commodities are positively and reliably related to both expected and unexpected inflation, both assets demonstrate levels of volatility that make them an ineffective inflation hedge. This can be seen in the chart below.

Source: Dimensional Fund Advisors (2022)

Why are commodities so volatile, compared to other assets? Well commodity prices are driven primarily by supply and demand factors, which can and do change frequently by considerable amounts. Some commodities have shown more stability than others, such as gold, but even this “safe” commodity has experienced periods of relatively high volatility.

Source: Bakas and Triantafyllou (2020)

Our Position

In light of the discussion above our portfolios do not contain commodity funds. However, we still maintain exposure to commodities indirectly because the funds we invest in, hold mining and commodity-producing companies. Therefore, our investors are well placed to benefit from commodity returns over the long term. Maintaining our global approach to investing also provides our investors with the best long-term hedge against inflation.

This article is produced by us for Financial Advisers who may choose to share it with their clients. Timeline & Betafolio do not offer direct-to-consumer products.

References

- Bakas, D., & Triantafyllou, A. (2020). Commodity Price Volatility and the Economic Uncertainty of Pandemics. Economics Letters, 193. Retrieved from http://repository.essex.ac.uk/27765/1/Bakas_Triantafyllou-2020_Commodity%20price%20volatility%20and%20the%20economic%20uncertainty%20of%20pandemics.pdf

- Dimensional Fund Advisors. (2022). Macroeconomic Indicators.

- US Global Investors. (2022, January 6). Periodic Table Of Commodities Returns 2021. Retrieved from US Global Investors: https://www.usfunds.com/resource/periodic-table-of-commodities-2021/#peri

- Vanguard. (2021). Economic and market outlook for 2022: Striking a better balance.