Overview & Valuation

Commodities are classed as “alternative” investments. Unlike “financial” or “traditional” assets such as bonds and equity, commodities are physical assets that produce no cashflows and may incur storage and transportation costs.

This makes determining the fair value of commodities difficult. In simple terms, the standard approach to valuing financial assets is to forecast all expected cashflows, be it interest payments or dividends. For each expected cashflow, we apply a “discount rate” based on the risk of the investment and increase the impact of this discount rate as cashflows extend further into the future. This gives us the current value of the investment.

Instead, values of commodities like oil, gold, or wheat are primarily influenced by supply and demand dynamics, including factors like weather, geopolitical events, and production changes. The two prices associated with commodities are the current, or “spot” price, which is the price for immediate delivery of goods, and the futures price, which is the price agreed upon for delivery at a future date. The spot price can be viewed as the discounted selling price of the commodity at some time in the future.

Storage costs for commodities often result in forward prices that become higher the longer the time until the commodity is due to be sold. This does not necessarily mean, however, that a commodity’s futures price is always higher than its spot price, because of expectations of future production and demand levels.

The simplest way an investor can gain exposure to commodities is to buy and hold the commodity themselves. This will not always be practical. Although some commodities are easy to buy and store (e.g., small quantities of gold), buying and storing gas or livestock would be difficult and expensive for most investors. Also, the investor would likely find it difficult to hold a diversified portfolio of commodities.

Because of this, one primary way investors gain diversified exposure to commodities is via commodity funds that invest in financial instruments called futures. Futures are, essentially, contracts that allow producers and buyers to lock in a price and remove uncertainty. For example, a farmer may wish to guarantee the price he receives for the grain that will be harvested next year.

At the same time, a baker may want to lock in the price he will pay for the grain to make bread. Each will enter into a futures contract today to agree on the price in the future. When this contract expires, if the current price in one year is not the same as the futures prices that were agreed by the buyer and seller, one will be worse off. For example, had the farmer agreed to sell his grain for £100 but a year later, grain in the market is trading at £250, the farmer effectively loses out by £150.

The commodity fund, essentially, speculates on the future price of commodities by forecasting supply and demand and then takes positions in futures contracts, hoping to benefit from those anticipated movements. Long-term results are based on the consistency and accuracy of the fund managers’ predictions.

It is important to understand that “commodities” includes a wide range of sectors, and although certain commodities, as a whole, may have performed well in comparison to bonds and equity in recent times, individual commodity sectors, over time, have not performed consistently. For obvious reasons, factors that influence supply and demand dynamics, thus influencing prices, differ for each commodity sector.

This chart serves to illustrate the inconsistency of returns between commodity sectors.

The Periodic Table of Commodities Returns 2023

Inflation Hedge?

Including commodities in investment portfolios is often advocated for two key reasons: diversification and inflation protection. The diversifying effect of commodities is easy to understand, as their prices often move independently from stocks and bonds. As for inflation protection, commodities can serve as a hedge because their prices typically rise with inflation (for instance, during periods of high inflation, oil prices often increase, due to the rising costs of production and extraction; the rise in oil prices would then drive up inflation even further). This means when the purchasing power of money decreases, the value of commodities held in a portfolio could increase, offsetting the inflationary loss in purchasing power.

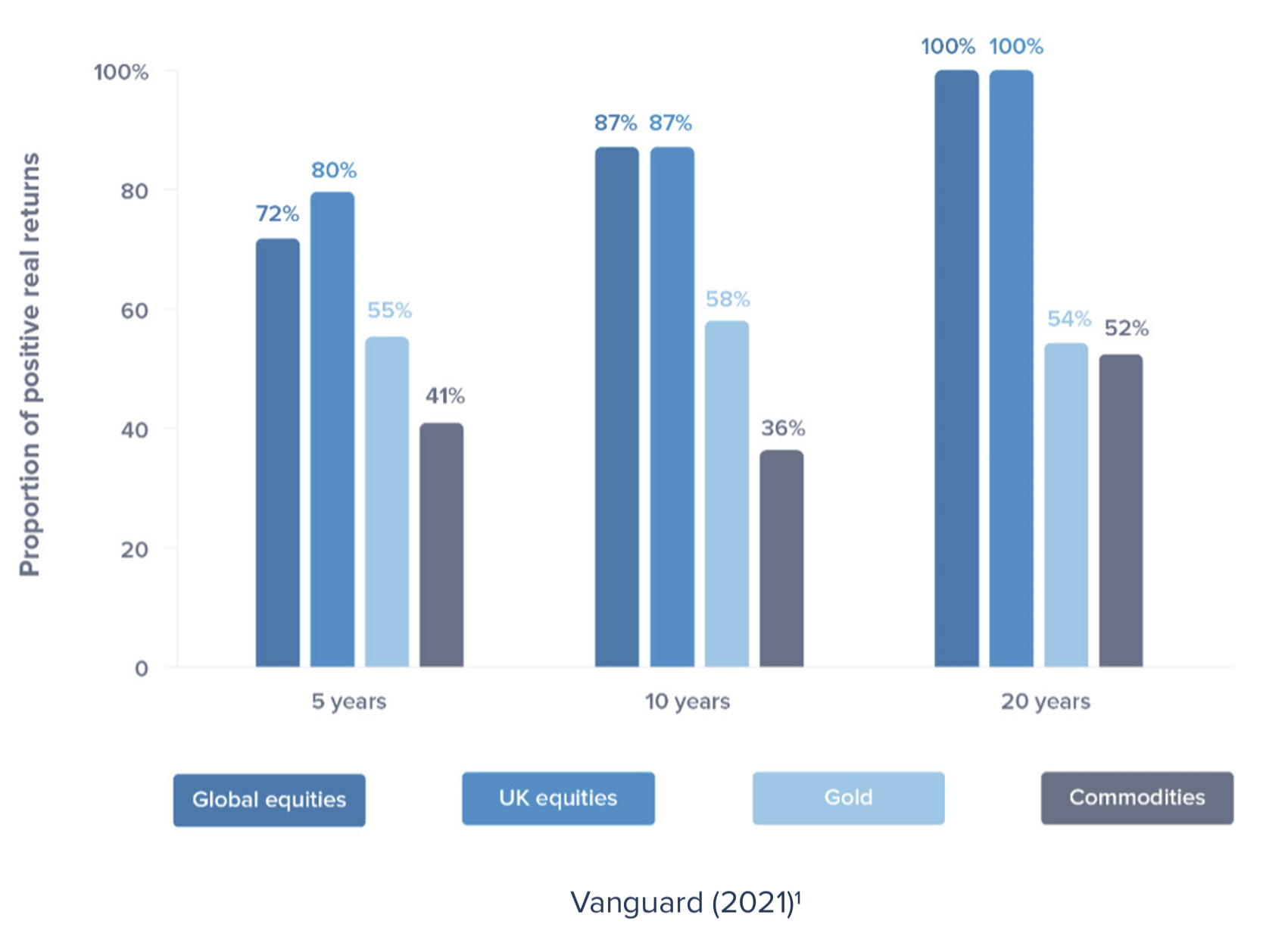

Are these investors who have traditionally seen commodities as a “hedge” against inflation right in their views? Yes and no. Over short-term horizons, studies have found that even a small allocation to commodities is effective at safeguarding the overall portfolio against unexpected inflation, while equities have not been a good inflation hedge. However, where equities come into their own, as is so often the case, is over the long term. If investors want to give themselves the best chance of growing their wealth, in excess of inflation, holding equities and enjoying the benefits of equity-risk premium is the best long-run strategy. This is reflected in the chart below. Over five-, 10-, and 20 year periods, the chance of achieving a positive real return is far higher by investing in equities rather than commodities.

Global equities have been most likely to beat inflation in the long term

The chart shows the proportion of real five-, 10- and 20-year returns that have been above 0%. The sample period for the monthly data is 31 January 1975 to 31 October 2021. Volatility is calculated over monthly returns of the entire sample period. Sources: Vanguard calculations in GBP, based on data from Bloomberg and the OECD.

Volatility of Returns for different asset classes

It’s not just the long-term returns of commodities compared to equities that make them less attractive as an inflation hedge, it’s also the volatility of returns. This can be seen in the chart above; commodities had the greatest volatility of returns over the 46-year sample period.

Why are commodities so volatile, compared to other assets? As explained, commodity prices are driven primarily by supply and demand factors, which can and do change frequently by considerable amounts. Some commodities have shown more stability than others, such as gold, but even this “safe” commodity has experienced periods of relatively high volatility.

Annualised volatility of gold price vs stock Index 1974 - 2024

When only looking at the near future, according to the IMF, commodity prices could become more volatile, due to increasing climate and geopolitical shocks. One trend is that national and regional governments have been designating metals and minerals as strategic resources, influencing or manipulating their supplies and prices across borders. The same goes for food and energy commodities, the trading of which are subject to continuing disruptions by politics and conflicts, such as the ongoing war in Ukraine.

As critical suppliers of both energy and food, Russia and Ukraine’s confrontation has led to significant supply disruptions. These have contributed to a worldwide cost-of-living crisis by propelling commodity prices to unprecedented highs. At first glance, this scenario may appear to present an opportunity for commodity investors. However, from a more nuanced perspective, geopolitical tensions of such magnitude greatly enhance commodity price volatility. This increased volatility and unpredictability complicates investors’ ability to make well-informed investment decisions and to secure positive returns.

Global commodity price indices (Russia launched full invasion in Feb 2022)

Our Position

In light of the discussion above, our portfolios do not contain commodity funds. However, we still maintain exposure to commodities indirectly because the funds we invest in contain mining and commodity-producing companies. Therefore, our investors are well placed to benefit from commodity returns over the long term. Maintaining our global approach to investing also provides our investors with the best long-term hedge against inflation.

References

Bakas, D., & Triantafyllou, A. (2020). Commodity Price Volatility and the Economic Uncertainty of Pandemics. Economics Letters, 193. Retrieved from http://repository.essex.ac.uk/27765/1/Bakas_Triantafyllou-2020_ Commodity%20price%20volatility%20and%20the%20economic%20uncertainty%20of%20pandemics.pdf

Dimensional Fund Advisors. (2022). Macroeconomic Indicators.

Gourinchas, P.-O. (2023). Risilient Global Economy Still Limping Along, with Growing Divergences . IMF Blog.

US Global Investors. (2022, January 6). Periodic Table Of Commodities Returns 2021. Retrieved from US Global Investors: https://www.usfunds.com/resource/periodic-table-of-commodities-2021/#peri

Vanguard. (2021). Economic and market outlook for 2022: Striking a better balance.

Vanguard. (2023). The (unexpected) inflation-fighting poewr of commodities.

Disclaimer

Timeline Planning is a product of Timelineapp Tech Limited. Registered in England. RC: 11405676. Timeline Portfolios is part of Timeline Holdings Limited (Company number 13266210) incorporated under the laws of England and Wales, and operates under the wholly owned regulated subsidiary Timeline Portfolios (Company number 11557205), which is authorised and regulated by the Financial Conduct Authority (firm reference number 840807).

This article has been created for information purposes only and has been compiled from sources believed to be reliable. None of Timeline, its directors, officers or employees accepts liability for any loss arising from the use hereof or reliance hereon or for any act or omission by any such person, or makes any representations as to its accuracy and completeness. This document does not constitute an offer or solicitation to invest, it is not advice or a personal recommendation nor does it take into account the particular investment objectives, financial situation or needs of individual clients and it is recommended that you seek advice concerning suitability from your investment adviser.

Investors are warned that past performance is not necessarily a guide to future performance, income is not guaranteed, share prices may go up or down and you may not get back the original capital invested. The value of your investment may also rise or fall due to changes in tax rates and rates of exchange if different to the currency in which you measure your wealth.

.png)