.png)

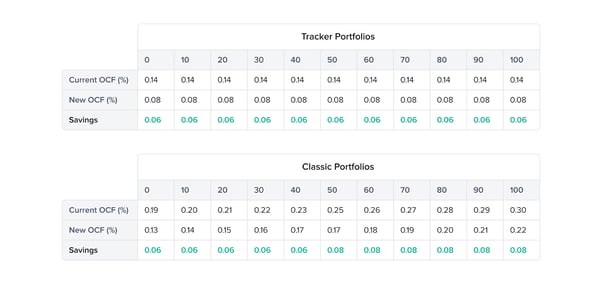

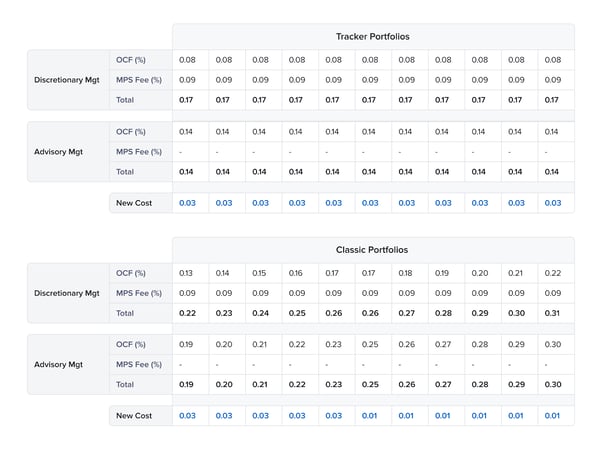

We recently unveiled a massive reduction in OCF for our portfolios. The OCF reduction of between 6 - 8bps across our portfolios translates to a whopping £800k a year in savings to the existing investors in our portfolios, a figure that will compound over the next few years.

Thanks to our incredible growth over the past ~3 years, we have been able to negotiate preferential institutional share classes with some of the world's biggest asset managers.

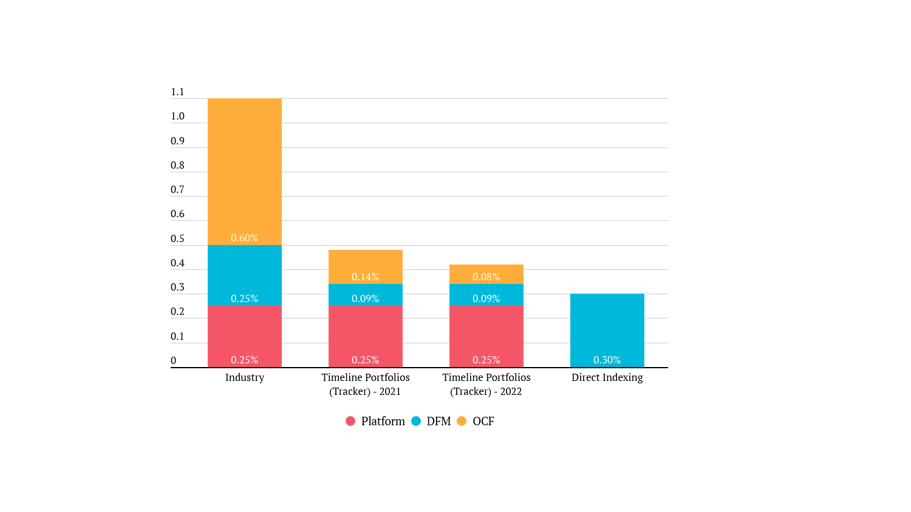

This means that our globally diversified Tracker portfolio with an OCF of 0.08%, plus our market-leading 0.09% for discretionary management is now available for a total of 0.17%! Not to mention that this comes with our integrated technology that includes Portfolio Analytics, Cashflow Planning, Risk Profiling and Factfind.

The inevitable result is that we are starting to displace overpriced DFMs and MPS providers peddling expensive portfolios. With this movement, we are making another giant stride towards this mission!

There is still much work to be done of course. I am firm in the belief that the adviser tech stack is disjointed, and needs shacking up.

Advisory Portfolios: A fool's errand?

Historically and justifiably, advisers shied away from using discretionary MPS on the basis it’s more expensive. I recall writing several articles decrying the insane value extraction by DFMs. But pontificating and complaining about something rarely brings change. So we saw the opportunity to use technology to bring this cost down significantly.

And now the tide is turning. With this reduction in OCF, we are effectively making running portfolios on an advisory basis redundant. In many cases we see, advisory portfolios are actually more expensive than Timeline portfolios. At the very least, it’s no cheaper to run advisory models.

We are now already at the point where the savings on OCF alone more or less covers the DFM fees, so that it is at least cost-neutral to clients. But when you add gains from drift-rebalancing vs calendar-driven rebalancing, the time-consuming process of advisory rebalancing and the abundant opportunities for error, it sounds like a fool’s errand to me. But I am biased of course. Do your own maths.

An Ode to Taking Chances

The name Lance Baron might not ring a bell to you. To me, he epitomises the forward-thinking financial advisers up and down the country daring to put their client interest first.

On a summer day in July 2019, I gave Lance an incoherent pitch at the top of The Shard about how we wanted to build a tech-enabled discretionary MPS provider that lowers cost for his clients and makes life easier for him as an adviser by removing the headaches and inefficiencies of portfolio management.

He peppered me with questions… most of which I answered poorly in hindsight. Still, Lance took a risk on us by agreeing to be the guinea pig for the discretionary MPS service. He put his reputation on the line and a few months later we soft-launched what is Timeline Portfolios today. And I am eternally grateful to him.

I can name a few other insanely brilliant advisers who backed us in the early days but I’d run out of space. Without them, we wouldn’t be here performing so strongly today.

To all the advisers out there striving to do the right things for their clients, this one's for you! 🥂